Making Business Financing & Government’s Schemes more accessible for Start-ups & MSMEs in India

MSMEmitra is utilising the power of technology and digital marketing for making business loans, funding, government promoted SME schemes for MSMEs and Start-up funding more accessible for entrepreneurs across India.

India has a population in excess of 1.30 Billion (and growing!!!). The country is the 6th largest and the fastest-growing trillion dollar economy in the world, making India one of the centres for innovation and disruption, with multiple untapped segments ripe for aggressive growth.

One such segment is the FINANCIAL SERVICES segment. While the market has been disrupted and stagnated over the last decade in the retail financial services (to be more precise, banking services for individuals), financial services for start-ups and small businesses have been deprived the same focus, until now.

START-UPS AND MSMEs — THE DRIVING FORCE BEHIND THE INDIAN ECONOMY

A staggering 95% of the total Industrial Units in India are classified as Micro, Small and Medium Enterprises (MSMEs or Micro and SMEs). India has over 42.50 Million MSME businesses, registered and unregistered, which employ over 80 Million people (close to 7% of the total population and around 40% of the total workforce). MSMEs in India contribute almost 50% to India’s manufacturing output and around 40% of the country’s total exports. 31.70% of the MSMEs manufacture close to 6,000 different products, while 68.20% are engaged in delivering various services.

Majority of the ideation, development, angel-funded, seed-funded and (some) Series-A stage start-ups are also classified as MSMEs because of falling under the threshold for Investments in Plant, Machinery and Equipment, thereby making them eligible for availing benefits applicable for MSMEs.

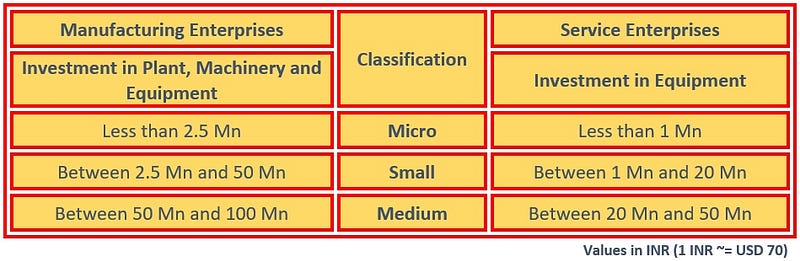

What is an MSME — In India, Micro, Small and Medium Enterprises are businesses whose investment in plant, machinery and equipment fall below a certain limit or within a particular range, as shown below:

The most common issues faced by Start-ups and MSMEs in India are:

· Lack of funding / financing at the right time; and

· Difficulty in availing the benefits of the applicable schemes and subsidies promoted by the Union Government of India.

While the government has initiated a number of funding related schemes (collateral free loans — CGTMSE, MUDRA, Startup India, Stand up India; and credit linked subsidies) for MSMEs in India through public sector and private sector Banks, and other financial institutions, the benefits of these schemes are hardly delivered to the target audience due to the lack of penetration and also due to a lack of interest in the private sector for promotion of these schemes.

SMALL BUSINESS FUNDING — SCOPE FOR DISRUPTION AND INNOVATION

Given the large number of small businesses in India and their contribution in the growth of the country, the SME financing segment (SME Loan, Business Loan, Startup Loan, etc) has a lot of potential and has opened new opportunities for the banking industry in India which is recovering from the burden of up to 15% Non-Performing Assets (NPAs) or Bad Loans, courtesy of the corporate lending (lending to large corporations) portfolio of Banks.

Lending to MSMEs (including eligible start-ups) mitigates the risk of bad loans to a large extent. A single loan of $1 Billion given to one large corporation will always have a higher risk of turning bad, as compared to loans of $500,000 given to 2,000 different businesses (not saying that banks should stop funding large corporations, but they can mitigate the risk of NPAs by having an equal exposure, distributed among the 42.50 Million smaller businesses).

While a number of steps have been undertaken by successive government to work on empowering the start-ups and MSMEs in India, the smaller businesses get left behind because they are not big enough to hire a full time CFO / CEO is often too involved in the business process to focus seriously on fundraising.

The other challenge is the understanding and compliance of the documentation process, including preparation of project report for bank loan.

Backed by the experience of over 40 years in Financial Services, the team at MSMEmitra helps small businesses in preparation of project report for bank loan and guides business through the documentation process for availing the loan.

Based on our research, we have also identified that Banks and NBFCs provide collateral free Unsecured Business Loans to existing and profitable small businesses at very competitive rates.

For a population in excess of 1.3 Billion (and growing) with a deep penetration of technology (through the availability of mobile phones and internet connections at dirt cheap rates), India has almost 800 Million Mobile phone users (close to 400 Million smartphone users). The average cost of 2 GB data at high speed (4-G / LTE) for a month is about USD 1.50 (or lower), making internet more accessible.

HOW A START-UP IS MAKING BUSINESS FINANCING MORE ACCESSIBLE FOR STARTUPS AND MSMEs

Taking the above statistics into consideration, MSMEmitra is focussing on using the power of digital marketing to make Business Financing more inclusive and accessible to the 42.50 Million MSMEs in India, by tying up with Industry-specific as well as segment-agnostic lending financial institutions.

MSMEs often find themselves in urgent need of funds for short-term requirements. The value that Unsecured Business Loans can create for the business is often much higher than the actual cost of financing.

Identifying this as a major area which can help businesses tide over short-term funding short-falls, MSMEmitra has tied up with multiple leading banks and financial institutions to offer Unsecured Business Loans, processed within 7 days without any collateral security.

In addition to quick processing and attractive interest rates and lower processing fees, MSMEmitra also offer 0.30% of the loan amount as Cashback after disbursal, to compensate (up to 50%) for the outgo on processing fees.

Similarly, MSMEmitra has tied up with a number of segment leading banks and financial institutions to offer collateral-based and collateral free SME Loan facilities for expansion and working capital requirements of businesses.

SME Loan facilities up to $275,000.00 (INR 20 Million) can be availed without collateral under MUDRA, CGTSME, Start-up India and Stand-up India Schemes, through any of the Scheduled Commercial Banks (Publc Sector, Private Sector and Foreign Banks).

Under these schemes, a guarantee, on behalf of the entrepreneurs is given to the Banks by the government-sponsored Trust at an annual premium of 0.5–1.00% of the loan amount. The interest rate, processing fees and charges on these loans are also capped at a fairly low level to ensure that entrepreneurs are not overburdened.

The interest in increasing their exposure under the collateral free SME loan schemes (where there’s a cap on interest rate) is bare minimum at the banks. However, Banks finance up to 70% value of properties under their MORTGAGE LOAN & COMMERCIAL PROPERTY PURCHASE LOANproducts.

These products help entrepreneurs in availing long-term loans at very low interest rates for any business related expenses.

MSMEmitra helps potential borrowers choose the most suitable mortgage loan and commercial property loan option through segment leading Banks and NBFCs.

Similar to the offerings on other loans, MSMEmitra also offers 0.30% of the loan amount as cashback after disbursal, to help cover for the cost on loan processing fees.

STARTUP AND SME SCHEMES FOR BUSINESSES IN INDIA

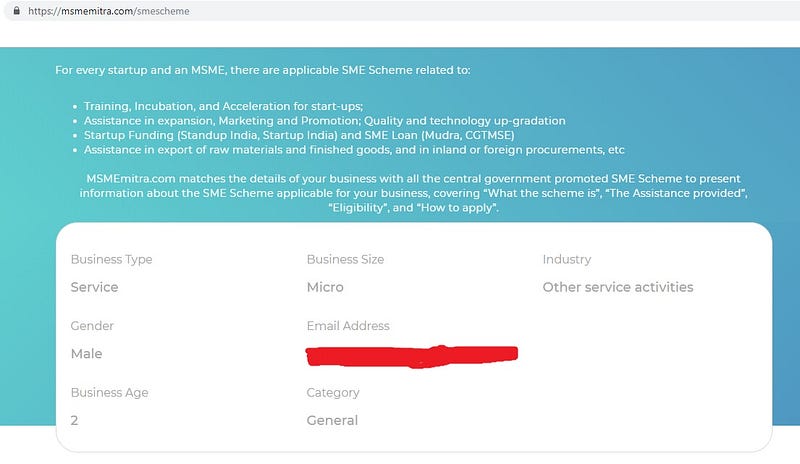

In our research while developing MSMEmitra.com, we found out that for every Start-up and MSME in India, there are at least 5 different government promoted schemes related to incubation, acceleration, expansion, funding, marketing and promotion, export, etc. However, identifying and availing the benefits of the applicable SME Scheme is nothing short of a nightmare.

At MSMEmitra.com, we developed an algorithm which matches the details of Start-ups and MSMEs with all the central government promoted SME schemes to present information about the business, promoter (founders) and industry specific applicable SME Schemes, covering “General Description”, “Eligibility” “Nature of Assistance”, and “How to apply”.

For example, for a business having the following profile, there are 10 different applicable SME Scheme

Within 2 minutes, entrepreneurs are able to identity SME Schemes specific to their business and need, and are educated about how to avail the benefits of the applicable SME Schemes.

To conclude, with plenty of other developments in the pipeline, MSMEmitra is hoping to be at the forefront of this shift in the growing success of Indian start-ups and small businesses.

—

ABOUT THE AUTHOR

Samved Bharadwaj is the Founder and Managing Partner of the bootstrapped Indian startup, MSMEmitra which he had co-founded with Ashish Jacob in August 2017. In the last 2 years, MSMEmitra has consulted and advised a number of start-ups and MSMEs and raised a cumulative total in excess of USD 1 Million (INR 70 Million) for its clients — Start-ups and MSMEs.

A young and dynamic team at MSMEmitra draws strength from the group’s experience of over 40 years in Financial Services, including Credit Reporting, Due Dilligence, Fundraising, B2B Debt Recovery, Banking, etc.

Disclaimer:

The views expressed in the article are the author’s own. The data in this write-up has been collated from various publicly available materials and secondary data, and MSMEmitra.com cannot guarantee the accuracy of the content. The opinions and expectations arrived at in this article, are based upon the analysis of the Industry by the author. Readers are requested to check the authenticity of the data at their end, before making any decisions with inherent financial risks.

Thanks for sharing this greate information aboute MSME.

ReplyDeleteGet full MSME details and Instant Udyog Aadhaar Registration Service.